Now that we have decided to use CollegeSure CDs to save for our daughter's college the question is – how? The answer turns out to be non-trivial in that we need to figure out how many CDs of what duration at what cost to buy each year between now and when she finishes college. After some experimentation I came up with an approach that seems to provide a reasonable cost and purchase plan. Below I explain how the approach works and provide a calculator that creates a purchase plan using the approach. Please keep in mind however that I'm no financial expert, that the code hasn't been properly tested and that objects may be closer than they appear.

Contents

2 How many units to buy

3 Defining the problem

4 Reverse Proportional Approach

5 Calculating DU

6 Calculating BMAX

7 Using the calculator

References

1 CollegeSure – buying one year at a time

The cheapest possible way to buy the CollegeSure CDs we need to pay for our daughter's education is to simply buy all 4 years worth now. Using the prices I got on 1/25/2008 the total cost would be $153,891.70 to buy 4 years, 1 unit a year. In theory we could raid our retirement investments to try and scrape up that much cash but I would rather leave our retirement funds alone. Especially since we can, if worst comes to worse, take out loans later to pay for our daughter's college but we really don't have a lot of options for rebuilding our retirement savings. Besides if we lock up the money in college savings now and our daughter doesn't go to college or goes to a cheaper college then we will have to pay all sorts of penalties to get the money out.

Given the various uncertainties I want to take my standard approach and spread the risk equally across the various years from now until our daughter is done with college. My standard approach is to figure out a constant sum of money, in inflation adjusted terms, to invest every year from now until our daughter is done with college. I don't claim the strategy is perfect but it's all I've got.

2 How many units to buy

So the bottom line seems to be that we will calculate the cost of buying 4 CDs (one for each year of college). The first step is to figure out how many units to buy. As previously explained one unit equals the average cost of one year's private college. But UCLA, my reference school, costs more than the average private college.

|

|

|

|

|

| School Year |

UCLA(out of state, undergraduate, Residence Halls) |

Ratio | |

|

|

|

|

|

|

|

|

|

|

| 2007-2008 |

$35,272 |

$43,481 |

1.23 |

|

|

|

|

|

| 2008-2009 |

$37,208 |

$45,743 |

1.23 |

|

|

|

|

|

So it seems I should plan on purchasing 1.23 units for each school year. Obviously this relationship can change over time and as it does I'll have to adjust the target units to purchase.

3 Defining the problem

But the real issue that caused me grief is – how should we calculate how much money to put into each CD? Given that I want to save the same amount of money each year (in inflation adjusted terms) I need to figure out how much money each year to spend on which CDs so that at the end we will have the right number of units for each year our daughter is going to college and will have spent the same amount of money each year on buying CDs.

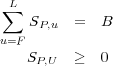

The first constraint is that we spend the same amount of money, in inflation adjusted terms, each year buying CDs. This can be expressed as:

Where P is the year that a CD is purchased, u is the college year the CD is intended to be used for, F is the first year of college, L is the last year of college and S represents the amount of money spent in year P on a CD to be used for year of college u. The goal then is for any given year of purchasing P the sum of the money spent on the CDs should equal to B where B, in inflation adjusted terms, is a constant. We also require that S always be 0 or higher since we are not going to short the CDs.

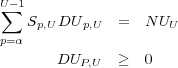

The second constraint is a function of our goal, to have enough the right number of CollegeCD units for each year of college our daughter will attend school.

Where α is the first year we would have purchased CDs and where DU represents how many units a dollar would buy in CollegeSure CDs purchased in year p for use in school year U. NU represents the number of units needed for year U. The summation term stops at U-1 because we can't buy a CD in the same college year it is to be used in. So the goal of the previous summation is that for any given college year U the total number of units purchased for that year will equal NUU.

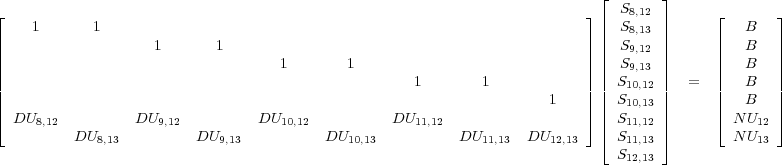

The previous is really just a series of linear equations. The trick then is to find the values for S that when put into the equations will meet both of the previous requirements. The only problem is that in the interesting case we have more variables than equations. Let's pretend that it's 2008 and our daughter was going to start school in 2012 and finish school in 2013. In that case we could express the system to be solved as:

Note: The empty spaces are 0s, I have left them out to make the matrix easier to read.

DU is known, this is the actual or estimated number of units a $1 could purchase in the given purchase year for the given school year. So DU8,12 represents how many units of CollegeSure CDs $1 could buy in the year 2008 for use in the school year 2012. DU can be assumed to express its value in constant dollars so we don't have to worry about adjusting for inflation. NU is also known, for example, in the previous section I calculated that NU would be 1.23 for both years. The trick then is find values for S so that when multipled by the left hand matrix the result is that for each year the spending equals to some constant B and we have exactly NU units worth of CDs available for the 2012 and 2013 school years. In this case we have 9 variables but only 7 equations which in this case happens to mean that there are many possible legal solutions. So how the heck do we find the 'optimal' values for S that will produce the lowest possible B and still result in having NU units for each year of college? This assumes, btw, that there even is a solution. In some cases there is no exact solution and we will have to violate the constraints to some extent in order to get a result.

4 Reverse Proportional Approach

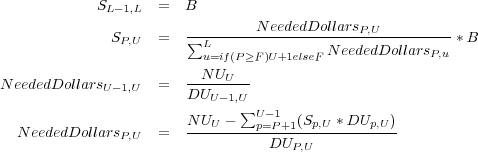

While playing with the math the best solution I could come up with for calculating the best purchase plan is what I call the reverse proportional approach. In this approach at each purchase year I spend the budget in proportion to how much money it would cost to purchase all the units needed for that school year. I start this process at the last purchase year and work backwards. The following equations describe the approach:

NeededDollars can be negative so I put in a check that returns 0 to cover that possibility in my code.

To calculate my purchase budget I start with an initial budget that I'm sure will be larger than I need (see BMAX later for details) and then start a linear search trying to find a value for B that produces a purchase budget that buys NU units worth of CDs for each college year.

I've tried a number of other approaches to finding a good purchase plan including Monte Carlo simulations and genetic algorithms but neither approach was able to produce a better solution than the reverse proportional approach. Unfortunately this means nothing in the universal scheme of things. Just because I can't find a better approach then the reverse proportional approach doesn't mean one doesn't exist. It just means that I, a complete amateur, couldn't do better.

5 Calculating DU

The DU function returns, for a given year of purchase and year of college, how many units $1 will buy. To calculate this value I start off with the cost of buying CollegeSure CDs quoted to me on 1/24/2008 and 1/25/2008. The question I asked CollegeSure was "If I gave you $1,000 today for a CollegeSure CD that will expire in year X how many units will I have bought?" For CDs purchased in 2008 this is the values they gave me:

|

|

|

|

| Year of Use | Units for $1000 | Imputed cost of 1 Unit |

|

|

|

|

|

|

|

|

| 2009 | .0269 |

$37,174.72

|

|

|

|

|

| 2010 | .0266 | $37,593.98 |

|

|

|

|

| 2011 | .0262 | $38,167.94 |

|

|

|

|

| 2012 | .0258 | $38,759.69 |

|

|

|

|

| 2013 | .0254 | $39,370.08 |

|

|

|

|

| 2014 | .0251 | $39,840.64 |

|

|

|

|

| 2015 | .0247 | $40,322.58 |

|

|

|

|

| 2016 | .0244 | $40,983.61 |

|

|

|

|

| 2017 | .0240 | $41,666.67 |

|

|

|

|

| 2018 | .0237 | $42,194.09 |

|

|

|

|

| 2019 | .0234 | $42,735.04 |

|

|

|

|

| 2020 | .0230 | $43,478.26 |

|

|

|

|

| 2021 | .0227 | $44,052.86 |

|

|

|

|

| 2022 | .0224 | $44,642.86 |

|

|

|

|

| 2023 | .0221 | $45,248.87 |

|

|

|

|

| 2024 | .0218 | $45,871.66 |

|

|

|

|

| 2025 | .0214 | $46,728.97 |

|

|

|

|

| 2026 | .0211 | $47,393.36 |

|

|

|

|

| 2027 | .0208 | $48,076.92 |

|

|

|

|

| 2028 | .0205 | $48,780.49 |

|

|

|

|

The previous table assumes that the year of purchase is 2008. I'm not going to worry about DU where the year of purchase is before 2008 since we aren't going to travel back in time. But I do have to worry about the value of DU when the year of purchase is greater than 2008. In that case I will assume that the values in the table given above hold but are adjusted by the yearly increase in college costs. This is a complete blind guess but I have to assume some sort of cost increase, above inflation, each year to compensate for the ever increasing cost of college.

![T-able[u---p--1] DUp,u = (1 + CI)p-2008](executingcollegesavings4x.png)

Where Table indexes into the previous table assuming that the first entry has the index value of 0. CI is the college cost increase and represents how much we expect college costs to go up each year. Previously I had calculated this value as 2.6% after inflation. I believe that CollegeSure CDs are actually available for maturities up to 22 years but I only asked for the values for up to 20 years which results in u-p having to be less than or equal to 19 in order to index into the table.

Also note that all calculations assume that one is buying on the date that the data in the table was recorded and that all future purchases will also be on that date. I haven't put in any kind of corrective when the purchase date and the table date is off. My intended solution to this problem is to get a new quote when I'm ready to buy. Yes, this has obvious issues if my buy dates are all different but given the timescale and uncertainties involved I don't care.

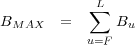

6 Calculating BMAX

Calculating a good initial guess for the upper bound in the linear search turns out to matter, a lot. If the value is lower than the actual minimal value then a correct result cannot be found. If the value is too much higher than the minimum value then it will take a long time for the linear search to find the result (a real issue in Javascript where the performance is typically pretty awful). While I was working on genetic algorithms to find the best portfolio I came up with a value called BMAX which represents the maximum theoretical yearly budget that would be guaranteed to spend enough money to buy the necessary number of units. The trick was that I wanted a BMAX that would be reasonably close to the 'best' value so as to reduce the search space.

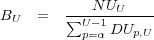

To calculate BMAX I used an approximation. Let's pretend I only needed to buy a single year's worth of college units. In that case solving the matrix above is trivial. Every year's budget (e.g. S) will be the exact same value. So I just need to calculate what budget, B (which all the S's equal to) will purchase 1 unit.

In other words the budget needed every year from year α to year U-1 for college year U (whichever that is) equals BU iff we are just saving for a single year. But I can use BU as a crude way of calculating BMAX.

7 Using the calculator

The calculator implements the reverse proportional approach. The calculator is fairly self explanatory. The key issue is that the data used to drive it is hopelessly out of date. I will contact the CollegeSure CD folks to get an update on the prices. If you have your own update you can download the file and do a search on the variable UnitsForDollars. It is an array that contains how many units a $1 can buy for a 1 year, 2 year, etc. CD.

In future years we can use the calculator by adjusting the units for each college year so they don't include the number of units we purchased this year. E.g. if we have already purchased Y units for college year X then we would enter NUX –Y units in the calculator for year X.