After looking at the various options available in 529 plans from stock mutual funds to bond mutual funds to age appropriate funds and so on the choice for us came down to TIPS mutual funds or CollegeSure CDs. We have decided to use CollegeSure CDs to save for our daughter's education. Yes, they have a horrible return and are quite possibly not FDIC insured (read the fine print) but of all the options this is the one that seems most reasonable.

Contents

2 Bond mutual funds

2.1 TIPS bond mutual funds

3 Bond like investments available in 529 plans

4 CollegeSure CD

4.1 Penalty for early withdrawal

5 Age Based Funds

6 Comparing the Top Two Contenders

7 And the Winner Is?

References

A Comparing CollegeSure CDs and TIPS Mutual Funds

B How Risky Are Bond Mutual Funds?

C But Doesn't Modern Portfolio Theory make stocks more reasonably predictable, at least in the aggregate?

Picking the right financial assets to save for college is a question of matching our needs to our financial assets. In this case we need to craft a portfolio designed to deliver a certain amount of money at a specified point in time.

1 No stocks

I like stocks. I know I shouldn't. I've studied enough of the international history of stock market movements to know that they are insanely risky and are most certainly not safer in the long run. But I like them. So when I started on this journey I was focused on what stocks and bonds to buy even though I knew this made little sense. The trap I fell into was not matching my assets to my liabilities. For example, if I am saving money for a fixed expense that will come due at a fixed point in the future does it make any sense to use an investment that makes absolutely no guarantees what so ever about how much it will return and when? If I was suggesting, say, using the income or some portion of a stock investment to pay for college that would be one thing. But because we are using a 529 plan all the money in the plan needs to go to education and therefore using stocks means believing that we can liquidate the entire portfolio at a fixed date and expect a predicable return. That simply isn't how stocks work so using stocks to save for college in a 529 plan just doesn't make sense to me.

2 Bond mutual funds

In many ways bonds would be a good match for college savings. They promise to pay a certain amount of money at a certain time. This is much better than, say, stocks. The problem is that I can't find any 529s that allow one to directly invest in traditional bonds. Instead the 529s offer bond mutual funds. A bond mutual fund is a different beast than buying and holding individual bonds to maturity. For one thing bond mutual funds make no promise about how much they will pay out. E.g. if I buy a 5% bond and hold it until maturity then I'm promised by the bond issuer to receive my 5% (subject to the risks explained in the TIPS bond mutual funds section below). A bond mutual fund makes no such promise. So fundamentally bond mutual funds aren't all that different than stocks in the sense that nobody is promising anything.

If our daughter is going to college in N years and we buy a bond with a N year maturity then in N years the bond matures, we get the principal and we move on with our lives. The amount of principal we get is set when we bought the bond. But if we need to sell the bond early, before its maturity, then we face interest rate risk. If market rates are higher than the bond's interest rate then we will have to sell the bond at a loss and lose some of our principal. This particular risk isn't an issue if we hold the bond to maturity.

But since bond mutual funds are essentially expiration free bonds whenever we need to pull out our money we have to face the very real risk of losing 'principal' (our initial investment) due to recent market movements. The risk of bad market movements taking a huge chunk out of the bond's value is quite real. For example, the Lehman Long Term Government Bond Index (which covers the kind of bonds I would imagine we would use to save for college) in 1999 went down 10.26% (after adjusting for inflation) in one year. This is a 10.26% loss in value due completely to interest rate risk (since the bonds themselves were still paying a positive return). Bonds have lots of risks but taking a 10% hair cut on the value of one's principal is (modulo general credit risk) not typically one of them.

Just to add insult to injury not only don't bond mutual funds have a well defined maturity but they also don't have a defined interest rate either. Normally one buys a bond at X% and gets X% repayments. It's not quite that simple since, outside of zero coupon bonds, there is re-investment risk. But with a bond mutual fund there is no defined interest rate which makes planning a nightmare. So my inclination is to avoid bond mutual funds as being incompatible with saving for a fixed expense at a fixed time.

BTW, much as with stocks, bond mutual funds can be an outstanding investment tool, especially given their benefits around diversification and a concurrent reduction in credit risk. I'm not panning stocks or bond mutual funds, I am however of the belief that they aren't the best investments to use to save for fixed expenses.

2.1 TIPS bond mutual funds

If I absolutely had to pick a bond mutual fund to invest in I would pick a Treasury Inflation Protected Securities (TIPS) bond mutual fund. TIPS are issued by the United States Government and have one special feature, their principal is adjusted for inflation. This means that (in theory anyway) TIPS don't suffer from inflation risk. Also, because they are issued by the U.S. Government, one can fairly say that they don't suffer from credit risk either1 . TIPS however do suffer from interest rate risk, this shows up both in terms of calculating re-investment value of interest earned while we hold the mutual fund as well as possible risk when selling the mutual fund.

To help me estimate the likely return on TIPS I took a look at my favorite TIPS bond mutual fund, the Vanguard TIPS fund. It's maturity is 10 years (meaning the average bond held by the fund will expire in 10 years). To help me get some idea of what kind of return I could be looking at I looked at the historical yearly returns for 10 year TIPS bonds provided by the United States Federal Reserve. Unfortunately the data only goes back to 2003 even though TIPS were introduced in 1997. The geometric average return from 2003-2006 would be 2.0%. Still, 4 years isn't much data to go on. So I decided to take the 10 year Treasury bond return, adjust for inflation, and see what that would have returned. In this case the government provides data going back to 1962. After adjusting for inflation the geometric average return from 1962-2006 was 2.77%. But to be fair we will be saving money for 18 years. So I decided to do something extremely unscientific and calculate the geometric average return for all overlapping 18 year periods and then take the arithmetic average of the result. The mean return of the 18 year periods was 3.09% with the worst 18 year period (1963-1980) returning 0.93% and the best 18 year period (1981-1998) returning 4.90%.

For me, for some completely irrational reason, 2% is a magic number. 8 of the 28 18 year periods would have returned less than 2.55% which, given the fund expense of the Vanguard funds in a 529 plan, is what I would need to get a 2% return after expenses. Of course all these numbers are just that, numbers. There is no way for me to know, even using these numbers, what actual return I would have gotten since the bonds the mutual fund will buy aren't purchased based on some mythical yearly rate but based on the market rate on the date they are purchased.

In the end I'm going to fudge and estimate that a TIPS mutual fund would return around 2%, which means a 1.45% return in a 529 account thanks to mutual fund expenses.

3 Bond like investments available in 529 plans

I can't really find a way to buy traditional bonds through a 529 plan but there are some bond like creatures available. I did a search for bond 'like' offerings in 529 plans available to residents of the state of Washington.

|

|

|

|

Guaranteed Return Option |

States Offering it |

|

|

|

|

|

|

|

CollegeSure CD |

Arizona & Montana |

|

|

|

|

TIAA-CREF 3% Guaranteed Return/Acacia Principal Plus Account |

Georgia, Idaho, Kentucky, Michigan, Minnesota, Mississippi, Oklahoma & Tennessee/Washington DC |

|

|

|

|

Principal Protection |

Louisiana/Illinois/Maine/North Carolina/Texas |

|

|

|

|

Fifth Third 529 CDs |

Ohio |

|

|

|

The CollegeSure CD is a very interesting beast and I will examine it on its own later in this article.

The TIAA-CREF Guaranteed Return plan gets described in various ways but I believe the basic deal is that it will return 3% and might return more. Each year it looks like TIAA-CREF declares an interest rate and guarantees it for that year. Acacia Principal Plus Account works the same way with a 0.15% fee on the return. A 3% return isn't enough to even keep up with inflation and while their declared rates have been higher it doesn't look like they have yet to go over 4%. This doesn't seem like a good idea.

The Louisiana plan provides a state guarantee that any money invested in the principal protection option cannot lose principal but there is no guarantee of the interest rate. Illinois, Maine and Texas are similar except the sponsoring state appears not to guarantee that principal won't be lost. The North Carolina fund is run by the state but it isn't clear to me if it is guaranteed by the state. These options might be interesting for holding money just before spending it on college bills but without any idea of the likely return it doesn't seem a useful option for long term savings.

The Fifth Third 529 CDs are super long term CDs, up to 12 years, with a guaranteed interest rate. Unfortunately the interest rate does not adjust for inflation, neither the normal kind nor college price inflation. When I wrote this they were offering APYs of 4% interest rates for up to 19 years which isn't bad for a FDIC insured investment but I'm way too skittish to sign up for that return given the future possibilities of inflation. So this option won't work for me either.

4 CollegeSure CD

The CollegeSure CD plan offered by the College Savings Bank is the most interesting option in my opinion. It uses the Independent College 500 Index (IC500) calculated by the College Board to track changes in private four year college costs in the U.S. The CD then guarantees a return that will match the increase in the IC500 index. Of course anything that sounds too good to be true usually is and this is no exception. The first thing to notice in their disclosure statement [Fund(2007)] is the number 1.50%. This number is mentioned on page 2 and what it represents is the profit margin. The way the CollegeSure CD works is that every year the CD grows in value by the same rate of growth as the IC500 minus 1.5%. However the CollegeSure CD is sold at a premium to its face value so this is supposed to make up for the 1.5% return that the College Savings Bank is taking for itself.

Still, a guaranteed return, especially once that tracks the IC500 is nothing to sneeze at. So this brings up the next question – how sure can I be that the College Savings Bank will meet its obligations? The College Savings Bank is very quick to point out that their CDs are FDIC insured. This means that if the bank goes belly up the FDIC will guarantee not only the initial principal but all interest earned up to the point that the bank went bankrupt. There are still a few problems. First, it wasn't clear to the College Saving Bank if their CDs would qualify for FDIC insurance so they got opinions from the FDIC saying that their CDs should be insured. Note I say 'should'. Section I of [Fund(2007)] discloses the fact that the FDIC has never actually said they absolutely would insure the CDs only that given the FDIC's current interpretations of various regulations that weren't really written to cover the CollegeSure CDs it was the opinion of the FDIC that the CDs should be covered. But an opinion isn't a promise. The only real way to be sure that the CollegeSure CDs are covered are either for explicit rules to be passed covering them or for College Savings Bank to default and to see if the FDIC covers them.

But even if I assume that the CDs are covered there is still the problem that if the College Savings Bank can't meet its promises then I could find myself in a long painful struggle with the FDIC to get my money back. More to the point, how can I be sure that the College Savings Bank can meet its promises? Section VI. explains who the College Savings Bank is, the answer being – they are a wholly owned subsidiary of Pacific Lifecorp, a life insurance company.

A.M. Best, Moody's, Fitch and Standard and Poor's rate Pacific Lifecorp.

|

|

|

|

| Rating Company | Rating for Pacific Lifecorp | Rating Date |

|

|

|

|

|

|

|

|

| A.M. Best | a+ | 6/14/2007 |

|

|

|

|

| Fitch | A+ | 8/3/2007 |

|

|

|

|

| Moody's | A3 | 9/2/2003 |

|

|

|

|

| Standard & Poor's | A | 9/2/2003 |

|

|

|

|

| Standard & Poor's | AAAL (For CollegeSure CD) | 3/12/1996 |

|

|

|

|

All the rating agencies use the same BB, BBB, A, AA and AAA rating scale for 'investment grade'. So an A is good but not great. The AAAL rating is just for the CollegeSure CD itself, independent of Pacific Lifecorp. The rating is actually AAA with an L meaning that the AAA only applies to the amount covered by FDIC insurance. In other words S&P, I think, is really saying "we think the FDIC will insure this product." Just to add to the fun the College Savings Bank itself makes its money by investing in 'high quality' adjustable rate mortgages (no you didn't read that wrong).

4.1 Penalty for early withdrawal

If we should need or want to cash in the CD early we face a number of penalties. The first penalty is that the guarantee that the CD will match the IC500's growth only applies if we hold the CD to maturity. If we cash it in early then we get the return equal to the IC500 – 1.5%. This guarantee matters because if college inflation is less than was estimated by the College Savings Bank when it issued a CD then the 1.5% profit margin will leave less value in the CD than is needed to buy one year of college. If the CD is held to maturity then College Savings Bank will pay off the difference, but if the CD is sold early then you get what you get. In addition any CD terminated within the first 3 years faces a 10% penalty, which then drops to 5% until the last year (for CDs that had an original maturity of greater than 3 years) when it is 1%.

5 Age Based Funds

There are also 'age appropriate' mutual funds. These funds are keyed to certain maturity dates and are supposed to use a combination of stocks and bonds that shift over time. The idea generally being to start off 'risky' with lots of stocks and as our daughter gets closer to college the fund automatically switches into bonds. As [Bodie and Clowes(2003)] points out this approach doesn't make sense even in theory much less practice. The funds act as mechanical clocks, at certain points they change the stock/bond mix in a precalculated way. But what if the stock market has a huge run up, would it make sense to change sooner to bonds? What if stocks, early on, do horribly, would it make sense to stay in stocks longer? These aren't choices these funds can make. More to the point, as I discussed previously both stocks and bond mutual funds have serious risk consequences that make me generally not favor them for savings purposes.

6 Comparing the Top Two Contenders

The two assets that really caught my attention are TIPS mutual funds and CollegeSure CDs. [Bodie and Clowes(2003)] in particular directly recommends using CollegeSure CDs. To help me choose what to do I want to get a sense of how much money we will have to spend for one versus the other.

CollegeSure CDs are purchased in units where one unit equals the average cost of one year's tuition, fees, room and board at a private college in the US as determined by the IC500. The idea being that if I buy 1 unit worth of CD this year then in X years when the CD matures I will get back the cash equivalent of 1 unit at current prices. I called up the College Savings Bank and found out that for the 2007 school year one unit has $35,272 worth of value.

In the case of TIPS my choice would be the Nevada 529 plan which uses the Vanguard TIPS fund with an expense fee of 0.55% (which is more than twice the 0.2% fee Vanguard charges for the fund outside of a 529 plan). This is the cheapest reputable TIPS fund I could find in a 529 plan.

Below is the output of comparing the costs of buying 1 unit of a CollegeSure CD as quoted by CollegeSure (note that prices fluctuate daily) and how much I believe I would have to buy in TIPS mutual fund shares to get the same result. In the case of TIPS I list two numbers, a straight calculation of how much I would have to save in TIPS to have the expected money needed to pay for college and also that number plus 15%. The 15% is my attempt to compensate for the fluctuations in TIPS interest rates so as to give me a guarantee roughly equal to CollegeSure's. See A for details on how I calculated the TIPS savings value and B for details on where the 15% number came from.

|

|

|

|

|

| College Years |

Quoted CollegeSure CD Cost on 1/25/2008 |

TIPS Savings |

TIPS Savings w/15% extra protection |

|

|

|

|

|

|

|

|

|

|

| 2024 |

$45,871.56 |

$42,721.88 |

$49,130.16 |

|

|

|

|

|

| 2025 |

$46,728.97 |

$43,206.16 |

$49,687.08 |

|

|

|

|

|

| 2026 |

$47,393.36 |

$43,695.93 |

$50,250.32 |

|

|

|

|

|

| 2027 |

$48,076.92 |

$44,191.25 |

$50,819.94 |

|

|

|

|

|

| 2028 |

$48,780.49 |

$44,692.18 |

$51,396.01 |

|

|

|

|

|

7 And the Winner Is?

Given the rampant uncertainties in all the various numbers I call the CollegeSure CD cost and the TIPS w/15% extra protection cost a tie. So the decision really comes down to – which one will let us sleep better at night? Should we pick the CollegeSure CD and worry about Pacific Lifecorp or the College Savings Bank going bust or should we use TIPS and worry about college costs going up faster than the 2.6% used in our calculations? In the end we picked the CollegeSure CDs. Having a 'guarantee' that a dollars worth of college savings we put in now will be worth a dollar in the future is more enticing then worrying about Pacific Lifecorp/College Savings Bank's financial state. Yes, I know, famous last words. But in finance you role the dice and take your chances.

References

[Bernstein(2000)] William Bernstein. The Intelligent Asset Allocator. McGraw-Hill, 2000. URL http://www.efficientfrontier.com/BOOK/title.shtml.

[Bodie and Clowes(2003)] Zvi Bodie and Michael J. Clowes. Worry-Free Investing: A Safe Approach to Achieving Your Lifetime Financial Goals. Prentice Hall/Financial Times, 2003. URL http://www.prenhall.com/worryfree/.

[Fund(2007)] Arizona Family College Savings Program Trust Fund. Collegesure 529 plan disclosure statement and privacy policy, 08 2007. URL http://arizona.collegesavings.com/pdfs/azofferingcirc.pdf.

[Malkiel(1996)] Burton G. Malkiel. A Random Walk Down Wall Street. W.W. Norton & Company, 1996.

[Mandelbrot and Hudson(2004)] Benoit Mandelbrot and Richard L. Hudson. The (MIS)BEHAVIOR OF MARKETS. Basic Books, 2004.

A Comparing CollegeSure CDs and TIPS Mutual Funds

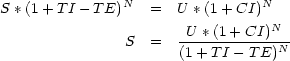

By way of background I will assume that college costs are going to go up by my previously estimated 2.6% a year. The cheapest TIPS mutual fund I could find is Nevada's Vanguard Fund which charges a 0.55% fee. Also, as previously mentioned, I will assume that the TIPS fund will make a real yearly return of 2%. So to calculate how much money I would have to save today in order to have one unit of value in N years the formula would be:

where S is the amount to be saved today and is the variable to be solved for. TI is the TIPS interest rate. TE is the expense ratio for the TIPS fund. U is the cost of a single unit in today's dollars. CI is the inflation rate for college costs. N is the number of years from now until our daughter goes to college. In our case TI = 2%, TE = 0.55%, U = $35,272 (e.q. IC500 unit cost for 2007), CI = 2.6% and N is range of values from 17 to 20. Note however that I'm being lazy. The CollegeSure CDs will expire in the middle of the year (when school starts) and not at the end of the year. So to make a fair comparison N should be at least calculated in months and the interest rates should be translated to monthly values. But I'm too lazy to do that work so my estimates will all be a bit off. But given all the other uncertainties this doesn't unduly worry me.

B How Risky Are Bond Mutual Funds?

|

|

|

|

| Bond Index (1995-2006) (all returns inflation adjusted) | Worst Single Year Return (year) | Geometric Yearly Average Return |

|

|

|

|

|

|

|

|

| Lehman Long Term Government Bond Index | -10.26% (1999) | 6.00% |

|

|

|

|

| Lehman Intermediate Term Government Bond Index | -5.49% (1999) | 4.75% |

|

|

|

|

| Lehman Short Term Government Bond Index | -2.08% (2005) | 3.32% |

|

|

|

|

| Lehman TIPS Bond Index (2001-2006) | -2.78% (2006) | 4.11% |

|

|

|

|

In the previous table I calculated the returns on various Lehman Brothers bond indexes. I admit the data is for a short period of time but finding bond index data has proven to be nearly mission impossible, the data above was taken from benchmarks that Vanguard uses for its bond index funds. If we had used, say, long term bonds to pay for our daughter's college fund then on the good side we would have seen a 6% real return but on the bad side we would have had to deal with watching up to 10% of the value of the portfolio vanish within a one year period because of interest rate changes. To be fair this was the worst year. The best year was 1995 when the index return 27.34% (and yes, that is inflation adjusted).

What I wondered is – how much more would we have to save in order to reasonably insulate ourselves from mark to market risk (the risk that interest rates will go against us when we need to liquidate our bond mutual fund position)? To answer this question I looked at duration. Duration is a measure of the interest rate sensitivity of a bond or bond mutual fund. A bond with a 2.2 year duration will be expected to go up by 2.2% if general interest rates go up 1% and down 2.2% if general interest rates go down 1%. At the time I write this the duration of the Vanguard TIPS mutual fund is 6.6 years. If that is the duration when I need to sell the bond then an interest rate change of 1% would change the value of my mutual fund shares by 6.6%.

To help me get some idea of what kind of volatility this implies in practice I got the results for 10 year treasury bonds, which seem to have a maturity roughly equal to the TIPS bonds from 1962-2006 and calculated the average yearly interest rate change. The simple average actually came out to 0.02% and standard deviation came out to 1.01%. The worst single year return was -2.95% which with a 6.6 year duration would mean a worst case scenario of losing 19.47% of the value of the portfolio in one year. But here's the really interesting part. If yearly interest rate changes do follow a normal distribution then given the mean and standard deviation a -2.95% change is 2.92 standard deviations out. To put this in perspective if the yearly interest rate changes follow a normal distribution then one would only expect to see a return that close to three standard deviations about twice every 1000 years or so. So my guess is, this puppy ain't normal. Of course I just proved beyond any shadow of a doubt that I'm no statistician. There are well defined tests to see if a distribution is normal within a certain confidence interval but it's been too many years between me and college statistics for me to remember how to do this test.

Lacking a better idea I'll randomly pick 2 standard deviations out or 2.02% which means 2.02 * 6.6 = 14.52%. So this means that if I want to use a TIPS bond fund to invest for our daughter's college education we need to 'over save' by 15% to make sure we can ride out any fluctuations in the interest rates in the market.

C But Doesn't Modern Portfolio Theory make stocks more reasonably predictable, at least in the aggregate?

My own encounter with personal finance really began with [Bernstein(2000)] and his explanation of modern portfolio theory (MPT). This naturally led to [Malkiel(1996)] which also extols the power and virtues of MPT. I mention MPT mostly because it provides a model to describe the expected behavior of stocks and so can be used to try and answer my basic questions about the suitability of an asset for savings. The only problem is that I am now convinced that MPT's core assumption isn't even approximately correct. This assumption is that stock returns can be estimated with a normal distribution. I later found out that it has been known since at least the 1960s that this simplification is wildly wrong. Thanks to work by folks like Mandelbrot (nicely summarized in [Mandelbrot and Hudson(2004)]) we know that stock returns do not follow a normal distribution. This devastates MPT because it means that the distributions and correlations that underly MPT's logic, and give me some basis of answering the basic risk/return questions, are just plain not true.

The situation is actually worse than it sounds because while the evidence seems, to me at least, to be clear that stocks don't fit a normal distribution I have not yet been able to find any compelling evidence as to what distribution stocks do follow. In fact, I'm beginning to seriously suspect that stocks do not follow any particular distribution on a consistent basis. Put another way, let's pretend stock returns did follow a normal distribution. But what if the shape of the distribution itself randomly changed in unpredictable but significant ways over time? Knowing that whatever distribution was used is normal would suddenly not be terribly useful.

I have personally reached a point where I have no clue what returns or volatility one should expect from stocks. What I am sure of, as excellent books like [Bodie and Clowes(2003)] explain, is that stocks are insanely volatile and that they are in fact not safer in the long run. That is, the probability of something 'really bad' happening to stock returns increases the longer one holds stock. Yes, one can argue that the opposite is also true, the longer one holds stocks the more likely something really good would happen but this actually goes to the heart of savings. Savings, in my mind, is about meeting a particular goal at a particular time. I don't know that I care that I exceed the goal, the priority is to at least meet it which means in the case of savings I'm more worried about loss than gain.

Given stock's unpredictable returns and high volatility there is absolutely no way to be sure that stocks will actually return what we need when we need it. In fact the only thing one seems to be able to be sure of with stocks is that there isn't much to be sure of. Nor are stocks even intending to provide any guarantee. The implicit deal with stocks is that in return for buying a piece of the company one gets to hold on for the ride and while promises are made (although not necessarily kept) that the ride will be, on average, better than it is worse, no promises are even attempted in terms of promising any kind of return over any kind of period. In other words stocks don't even pretend to be predictable.

So while I think there is a lot of logic in purchasing stocks as an investment2 buying stocks for a fixed savings goal like college looks little better than buying a lottery ticket. So I will be avoiding stocks in our college portfolio.